Self-Employed Affordability Mortgage: How Brokers Assess Income in the UK

TL;DR

- Self-employed affordability assessments are complex and time-intensive

- Brokers must interpret net profit vs salary/dividends and align with lender-specific affordability

- Traditional workflows are fragmented and manual

- AI tools streamline income analysis and documentation

- Brokers using modern workflows are significantly increasing capacity and efficiency

Introduction

Assessing a self-employed affordability mortgage is one of the most complex responsibilities for UK mortgage brokers.

Unlike PAYE applicants, self-employed cases require:

- Interpreting net profit vs salary/dividends

- Reviewing Qualified Accountant certificates

- Aligning with lender-specific affordability models

At the same time, brokers are under pressure to deliver faster decisions while maintaining compliance accuracy.

The Changing Landscape of Mortgage Affordability Assessment

The UK mortgage landscape is evolving rapidly:

- Over 4.2 million self-employed individuals

- Increasingly complex lending criteria

- Higher expectations for speed and transparency

This creates a key tension:

More complexity but less time to process it

What Types of Tools Exist Today?

Manual Assessment Methods

Strengths:

- Full control

- Flexibility

Limitations:

- Time-heavy

- Error-prone

- Hard to scale

Basic Digital Calculators

Strengths:

- Faster calculations

- Standardisation

Limitations:

- Limited handling of self-employed complexity

- No contextual understanding

- Manual data input

CRM + Spreadsheet Workflows

Strengths:

- Centralised data

- Custom workflows

Limitations:

- Fragmentation

- Manual syncing

- Weak integrations

Strengths Brokers Commonly Appreciate

- Structured frameworks

- Control over decisions

- Consistency in outputs

Recurring Limitations & Friction Points

- Manual interpretation of income

- Difficulty aligning with lender rules

- Repetitive admin work

- Lack of real-time insights

- Increased compliance pressure

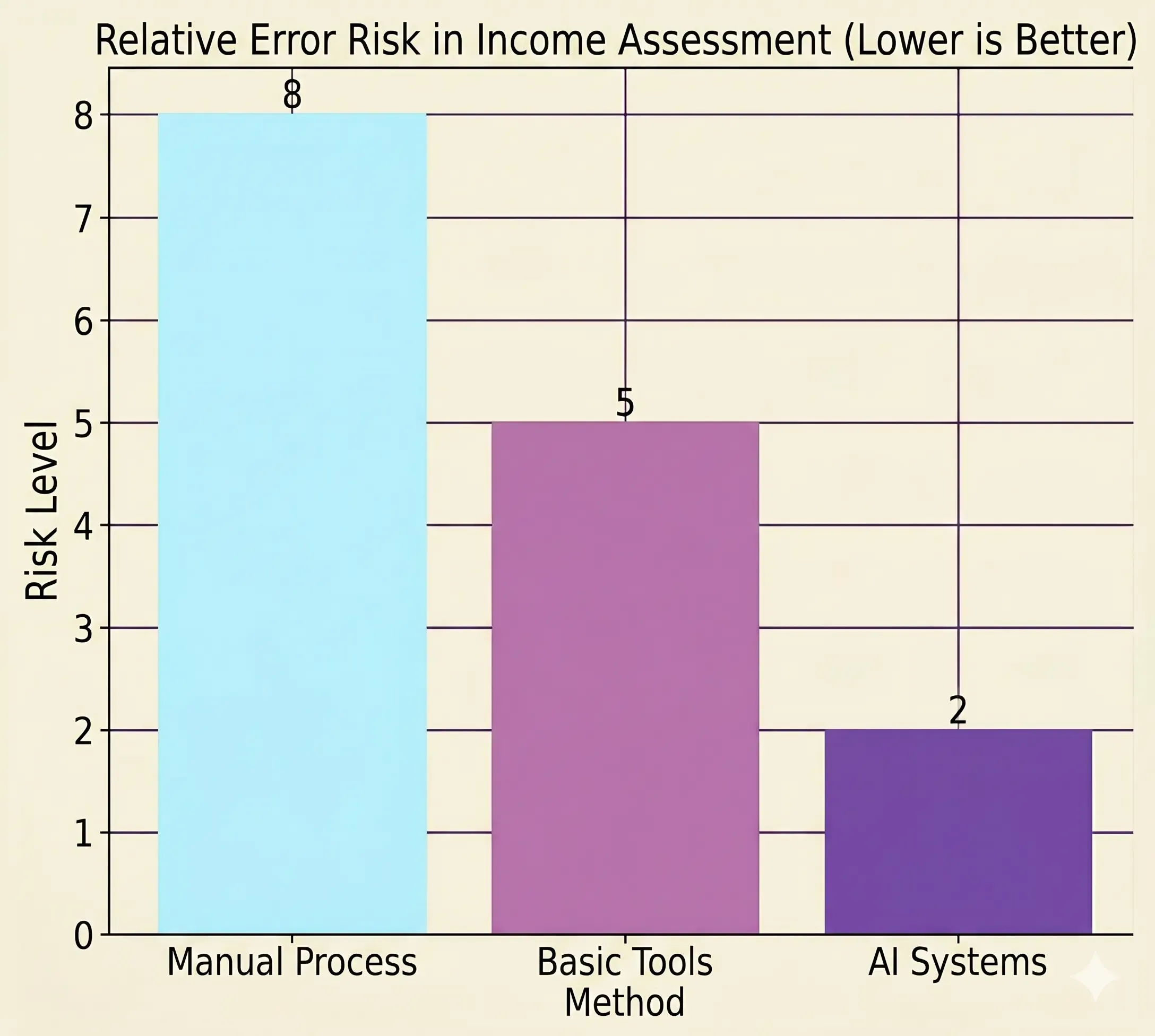

Error Risk in Income Assessment

Manual workflows increase risk due to inconsistent interpretation across documents and lender criteria.

A Practical Problem Many Brokers Encounter

The Self-Employed Income Puzzle

A broker receives:

- 2-3 years of accounts

- Fluctuating income

- Mixed salary/dividend structure

They must determine:

- Sustainable income

- Lender fit

- Compliance justification

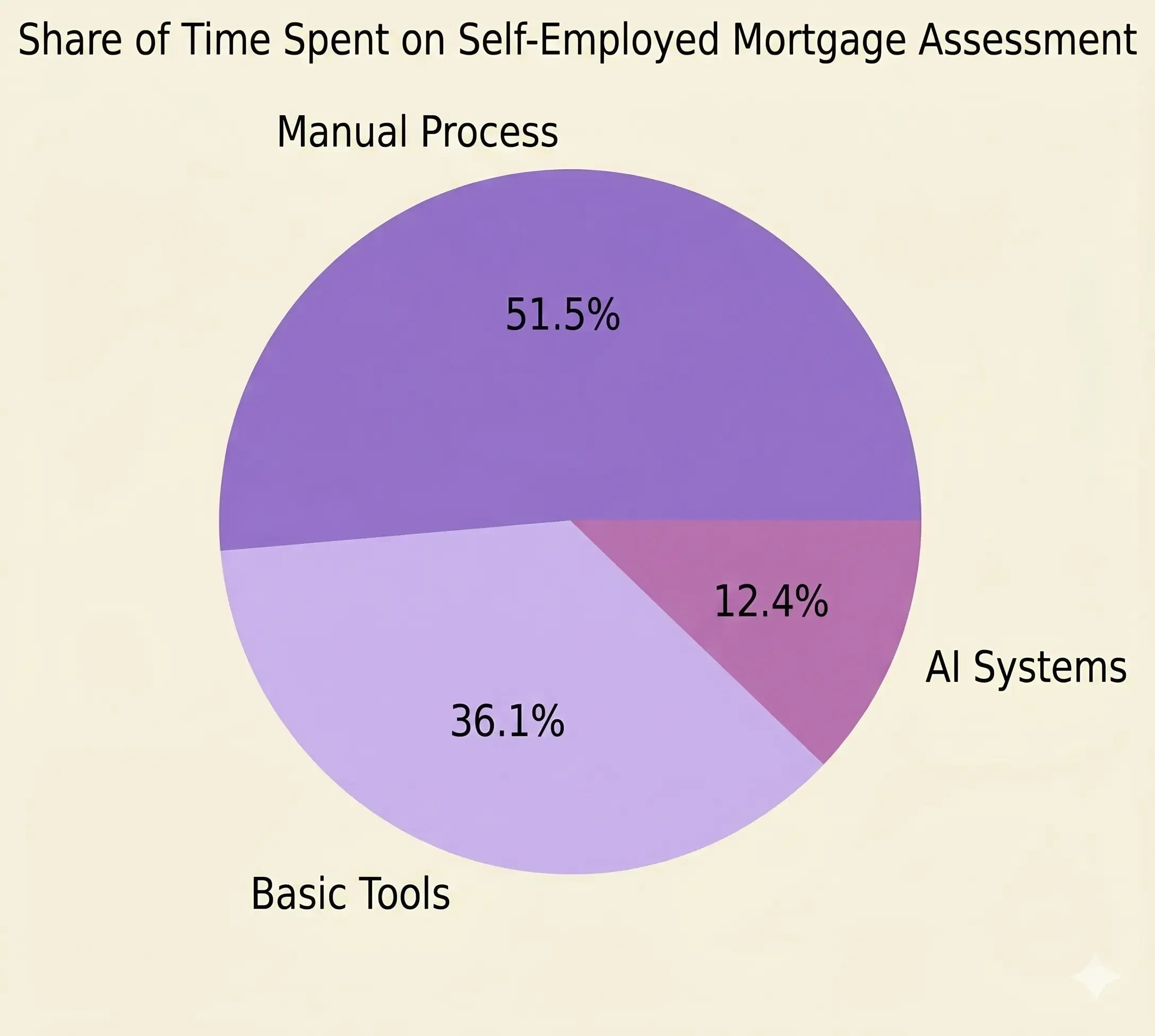

Time Distribution

Over 50% of time is spent on manual analysis.

Impact

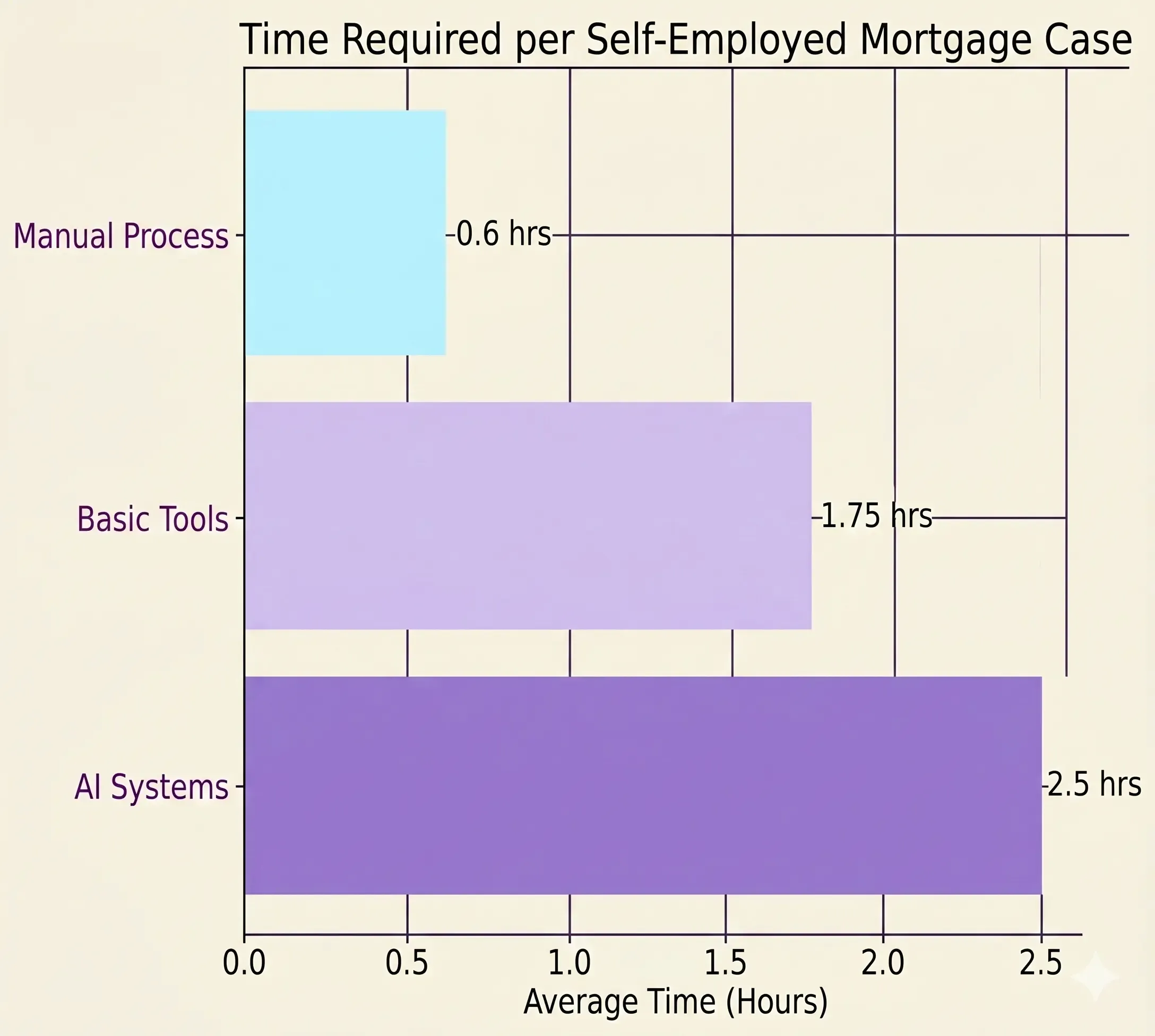

- 2-3 hours per case

- Slower turnaround

- Higher stress

- Increased error exposure

What Brokers Often Need But Struggle to Find

- Automated income structuring

- Real-time affordability insights

- Reduced manual workload

- Better workflow visibility

How Modern AI-Driven Systems Address This Gap

Modern workflows shift from manual interpretation → structured intelligence

Example: Automated Income Structuring

Instead of manually interpreting:

- SA302s

- Accountant certificates

- Tax calculations

AI-driven workflows produce:

- Clean, structured income summaries

- Clear breakdown of salary vs dividends

- Highlighted trends across years

What Brokers Actually Get

Imagine receiving a clean, structured income report that includes:

- Year-by-year income breakdown

- Automatically calculated averages

- Flags for declining or inconsistent income

- Lender-ready formatting

Instead of raw documents, brokers see:

- A ready-to-use affordability snapshot

- A client-ready explanation format

- A compliance-friendly structure

This is the real shift not just faster processing, but better outputs.

Example: Smart Affordability Modelling

- Scenario-based affordability outputs

- Alignment with lender-specific rules

- Instant comparisons

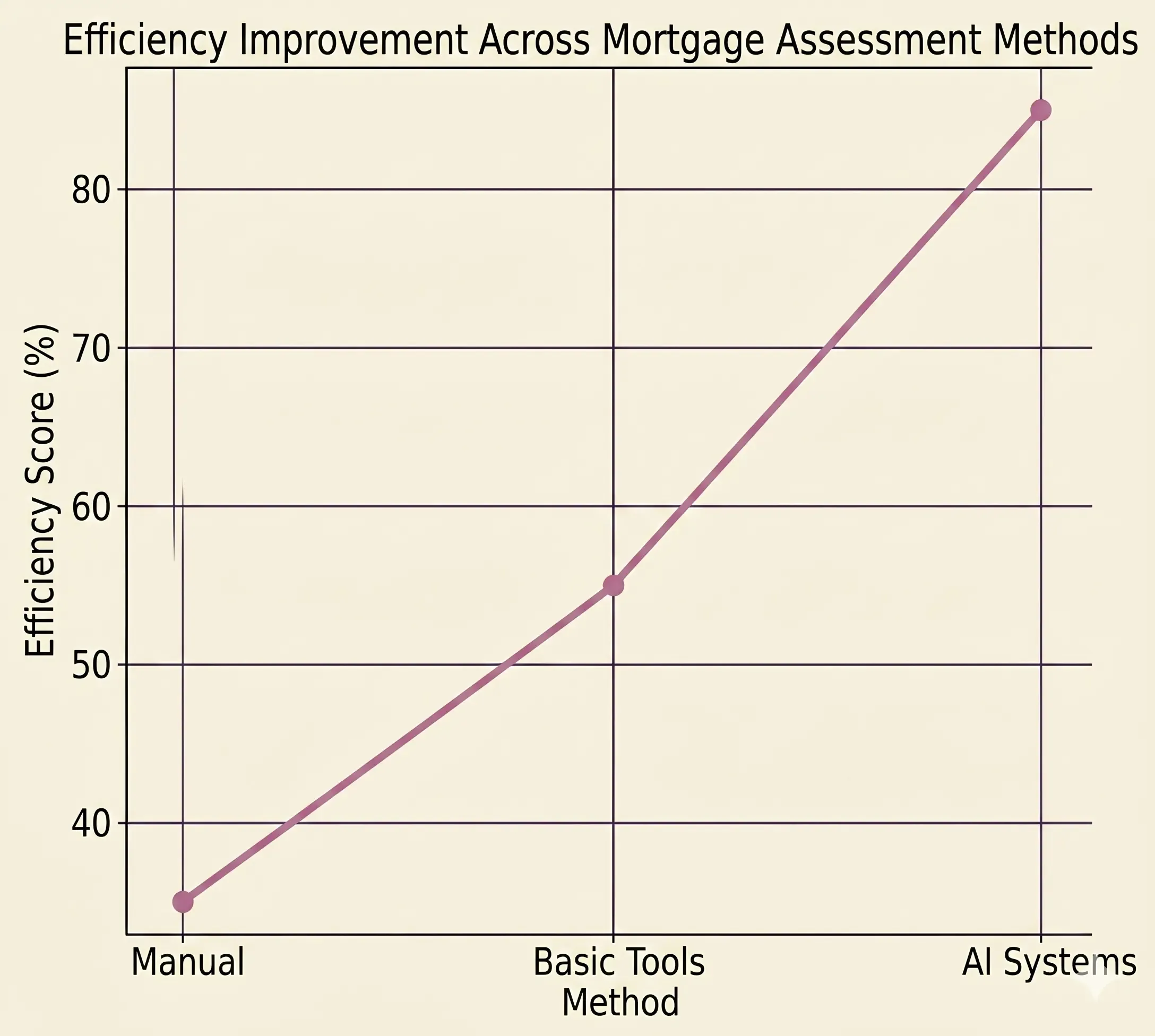

Efficiency Improvement

Efficiency improves significantly with AI-assisted workflows.

Where Spently & Draftlee Fit In

- Financial data is structured automatically

- Documentation is standardised and consistent

- Case-building becomes faster and clearer

Social Proof

“Mortgage advisors often say that moving to an AI-driven workflow isn't just about speed it's about having confidence that compliance documentation is consistently accurate and reliable.”

FOMO Insight

Brokers using modern AI-driven workflows are already reporting up to 3x increases in case capacity without increasing team size.

Real-Life Example

Scenario: Self-Employed Contractor

Traditional Workflow

- Manual review

- Spreadsheet calculations

- Manual documentation

Time: 2-3 hours

With AI-Assisted Workflow

- Automated income structuring

- Instant insights

- Pre-built documentation

Time: 30-45 minutes

Time Comparison

Up to 70-80% reduction in processing time

See It in Action

See Spently in Action - Book a 10-Min Demo

How to Choose Mortgage Affordability Tools

Ask:

- Does it reduce manual work or just shift it?

- Can it handle self-employed complexity?

- Does it support lender-specific rules?

- Where are the limitations?

Practical Considerations

- Integration capabilities

- Ease of use

- Accuracy

- Scalability

- Compliance alignment

Comparison of Tool Types

Key Takeaways

- Self-employed affordability is complex

- Traditional workflows are inefficient

- Brokers need better integration and automation

- AI enhances speed, accuracy, and consistency

- Early adopters are gaining a competitive edge

FAQ

How do brokers assess self-employed income?

Using SA302s, tax overviews, and accountant-certified documents.

What is lender-specific affordability?

Each lender applies unique rules when assessing income and risk.

Why is net profit vs dividends important?

It determines how income is treated in affordability calculations.

Can AI improve mortgage assessments?

Yes by automating data extraction and improving decision accuracy.

Is this the future of mortgage broking?

Increasingly, yes, especially for handling complex cases at scale.

Conclusion

The self-employed affordability mortgage process is evolving quickly.

Brokers who continue relying on manual workflows will face increasing pressure while those adopting smarter systems will gain:

- Speed

- Accuracy

- Scalability

The shift isn't coming. It's already happening!

Ready to see MAT in action?

Join mortgage professionals already using AI to grow their business.

Book a free demo