How to Scale Portfolio Landlord Cases: 3 Tools to Save 60% Admin Time in 2026

TL;DR (Quick Summary)

- Portfolio landlord mortgages are more complex in 2026 due to FCA Consumer Duty and new regulations

- Manual processes cost brokers £200+ per case in lost time

- Traditional tools create inefficiencies and compliance risks

- Modern solutions like myCriteria and Spently enable faster, smarter lender matching

- Brokers using smarter workflows report up to 60%-time savings

Join 500+ UK mortgage brokers saving an average of 4.5 hours per week

Introduction

In 2026, a 5-property portfolio case shouldn't take 5 hours to place.

Yet for many UK mortgage brokers, that's still the reality.

Portfolio landlord mortgages now demand deeper analysis, stricter compliance, and faster turnaround especially under FCA Consumer Duty and legislative changes like the Renters' Rights Bill.

500+ UK brokers are already saving 4.5+ hours per week using smarter workflows

Portfolio Efficiency at a Glance

- Time Saved: 60% per application

- Cost Recovered: £200+ per case

- Compliance: 100% automated audit trail

The Changing Landscape of Portfolio Landlord Mortgages

- Stricter lender criteria

- FCA Consumer Duty requiring clear justification of advice

- Renters' Rights Bill increasing scrutiny on tenancy structures

- Rising client expectations

2026 Reality:

Brokers must now demonstrate why a lender was selected not just present options.

A Practical Problem Many Brokers Encounter

Managing a landlord with 5-10 properties require:

- Manual lender comparisons

- Spreadsheet-based analysis

- Rewriting suitability reports

The Cost of Inaction

Based on an average broker hourly rate of £70:

- 3 hours per case = £210 lost per application

Annual impact:

- 10 cases/month → £2,100

- Yearly → £25,000+ lost productivity

The Anatomy of an Intelligent Portfolio Workflow

Since portfolio cases are rarely "simple," your toolkit shouldn't be either. Here is how the system processes a multi-property case to provide instant clarity:

1. The Unified Portfolio View

Instead of toggling between tabs or spreadsheets, the system aggregates all properties into a single, structured dashboard.

- The Benefit: Instantly see total LTV, aggregated rental cover, and overall portfolio yield across the entire client profile.

2. Multi-Lender Criteria Engine

The system runs your client's data against thousands of live criteria points simultaneously including 2026-specific stress tests.

- The Benefit: Receive a pre-filtered lender shortlist that accounts for complex property types (HMOs/MUBs) and specific income structures.

3. The "Suitability Logic" Generator

The system captures the reasoning behind every match, the "why" that the FCA requires under Consumer Duty.

- The Benefit: This rationale is exported directly into your Suitability Report, saving an extra 20-30 minutes of manual typing per case.

This is where the shift happens from hours of manual research to instant, decision-ready outputs.

Before vs After

Result: Faster decisions, fewer errors, built-in compliance

How Modern AI-Driven Systems Address This Gap

Example: Criteria-Based Matching (myCriteria)

- Input client + portfolio once

- System filters lenders instantly

- Matches based on real criteria

Key Advantage

The system doesn't just find a lender—it captures the reasoning behind the match.

This reasoning is exported directly into your Suitability Report, saving 20-30 minutes per case.

Example: Smart Deal Structuring (Spently)

- Organises multi-property scenarios

- Provides structured comparisons

- Improves decision clarity

Technical Insight

Modern systems:

- Use structured data + rules engines

- Automate lender matching

- Generate audit trails and suitability logic instantly

Real-Life Example

Scenario: 5-property refinance

Before

- 3 hours manual work

- Spreadsheet tracking

- Rewriting suitability reports

After (myCriteria + Spently)

- Data entered once

- Instant shortlist

- Auto-generated rationale

Outcome

- 60% faster

- Better client experience

- Compliance-ready instantly

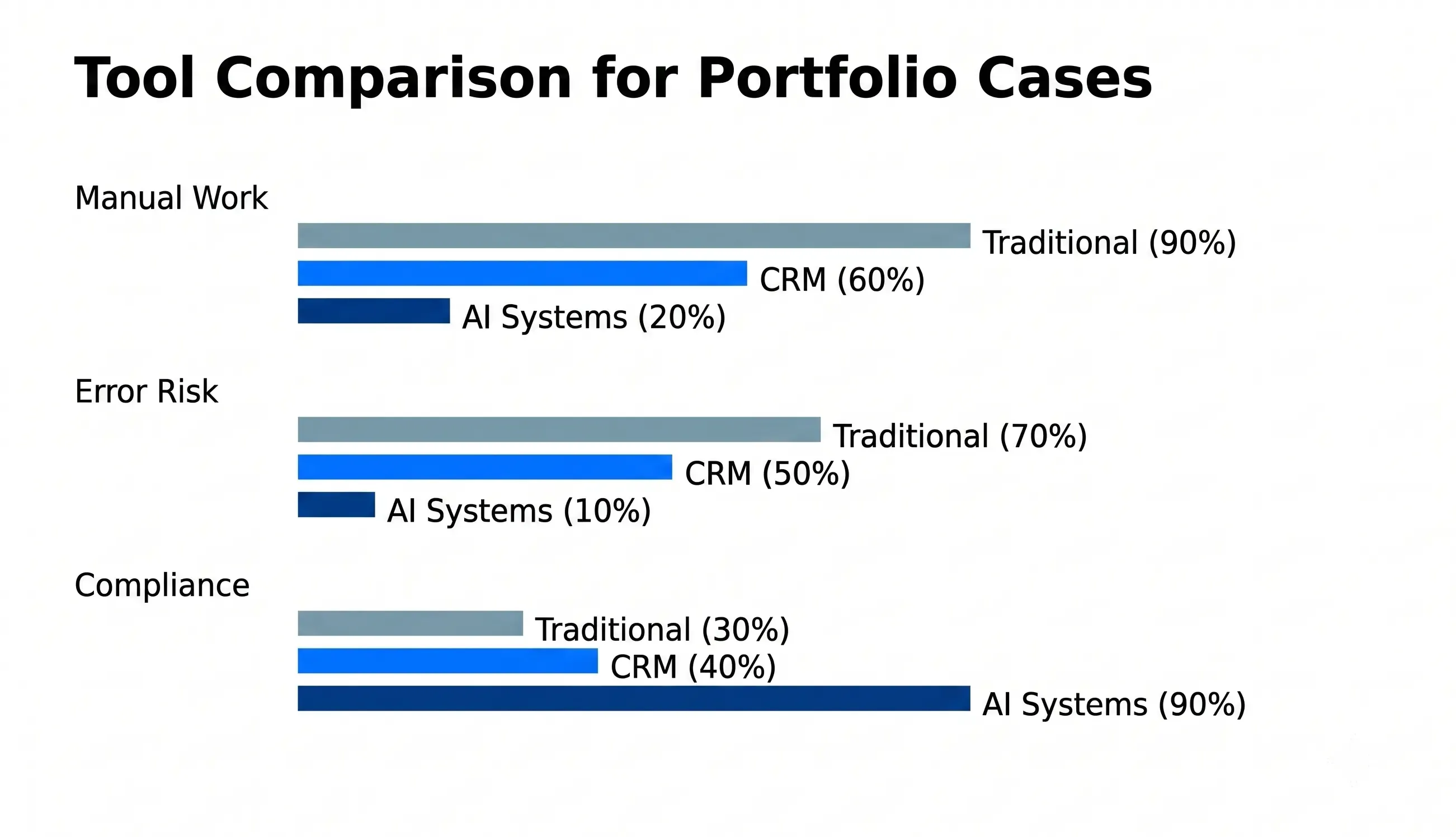

Comparison of Common Tool Characteristics

This chart highlights the operational difference between traditional methods, CRM systems, and modern AI-driven tools when handling portfolio landlord mortgage cases.

- Manual Work: Traditional methods rely heavily on manual input (90%), while AI tools reduce this to just 20%

- Error Risk: Human error drops significantly—from 70% with manual processes to just 10% with automated systems

- Compliance Readiness: AI-driven tools provide strong compliance support (90%), compared to limited support from older methods

Key takeaway:

Modern systems don't just improve one part of the workflow they simultaneously reduce workload, minimise risk, and strengthen compliance, making them far more efficient for handling complex portfolio cases.

Conclusion

Portfolio landlord mortgages in 2026 demand:

- Speed

- Accuracy

- Compliance clarity

The brokers who adopt smarter workflows will win, not just in efficiency, but in client trust and conversion.

Ready to Streamline Your Workflow?

Book a Demo of the Mortgage AI Toolkit

Start Your Free Trial

FAQs

1. What is a portfolio landlord mortgage?

A mortgage for landlords with 4+ mortgaged properties, requiring deeper affordability checks.

2. Why are these cases more complex in 2026?

Beyond the standard 4-property rule, the Renters' Rights Bill forces lenders to scrutinize rental security and periodic tenancies more closely. Manual stress-testing for these variables is now a major bottleneck—alongside FCA Consumer Duty requirements.

3. How much time do brokers spend on these cases?

Typically, 2-4 hours per case using traditional workflows.

4. What's the biggest inefficiency?

Manual lender matching and rewriting suitability reports.

5. How do myCriteria and Spently help?

They automate lender matching, structure portfolio data, and generate compliance-ready reasoning—saving time and reducing risk

Book a Demo →

Ready to see MAT in action?

Join mortgage professionals already using AI to grow their business.

Book a free demo