Mortgage Broker CRM vs Case Management: Key Differences UK Brokers Must Understand

TL;DR

Many UK mortgage firms assume their mortgage CRM covers everything.

It doesn't.

A CRM manages relationships and leads.

Case management software tracks applications and documentation.

But neither fully addresses internal oversight, FCA compliance tracking, adviser performance monitoring, or HR-linked revenue intelligence.

Understanding the difference between Mortgage Broker CRM vs Case Management is critical in 2026 especially for growing UK firms operating under Consumer Duty.

Introduction: Why This Distinction Matters in the UK Market

The UK mortgage industry remains heavily regulated and operationally complex.

According to UK Finance, gross mortgage lending exceeded £226 billion in 2023, with thousands of advisers operating under FCA supervision.

With Consumer Duty firmly embedded, firms must evidence:

- Clear communication and client understanding (Consumer Support outcome)

- Fair value for services delivered (Price & Value outcome)

- Ongoing oversight of adviser competency

- Structured governance and supervision

Many brokers rely on a mortgage CRM and a separate case management system. But confusion often arises:

- What does each system actually do?

- Where does compliance responsibility sit?

- Who monitors adviser performance?

- How do we evidence Consumer Duty outcomes?

Understanding Mortgage Broker CRM vs Case Management isn't just technical, it directly affects regulatory exposure, operational efficiency, and growth.

The Changing Operational Landscape for UK Brokers

Mortgage broker firms today typically operate with:

- A mortgage CRM

- A case management system

- A criteria search tool

- Compliance spreadsheets

- Manual HR tracking

- CPD logs stored separately

As firms scale, this fragmented setup creates blind spots.

The challenge isn't lack of tools.

It's lack of integration between:

- Lead capture

- Case progression

- Adviser accountability

- Compliance documentation

- Internal performance oversight

What Is a Mortgage CRM?

A mortgage CRM is a system designed to manage client relationships, enquiries, and communication throughout the sales pipeline.

It is primarily designed to:

- Store client data

- Track enquiries and leads

- Manage communication history

- Send reminders

- Organise pipeline stages

Strengths of a Mortgage CRM

Limitations of a Mortgage CRM

- Limited document progression tracking

- Minimal underwriting-stage visibility

- Often reactive rather than workflow-driven

- Does not manage internal compliance oversight

- Rarely integrates HR or CPD monitoring

A CRM is excellent for managing relationships.

It is not built to manage operational case complexity, adviser supervision, or Consumer Duty evidence tracking.

What Is Mortgage Case Management Software?

Mortgage case management software is designed to track and manage the lifecycle of a mortgage application from fact-find to completion.

It focuses on:

- Fact-find completion

- Document uploads

- Lender submission tracking

- Milestone progression

- Compliance document storage

Strengths of Case Management Systems

Limitations of Case Management Software

- Does not manage lead quality

- Limited adviser performance oversight

- Rarely tracks FCA CPD requirements

- No HR integration

- Often disconnected from revenue intelligence

Case management focuses on cases.

It does not focus on people performance, structured governance, or evidencing Consumer Duty outcomes like fair value and ongoing support.

Mortgage Broker CRM vs Case Management: Core Differences

This is where many UK firms unknowingly operate with risk exposure.

The Overlooked Layer: Internal Compliance & Adviser Oversight

Under FCA expectations and Consumer Duty principles, firms must demonstrate:

- Ongoing supervision

- Competency monitoring

- Training records

- Structured governance

- Evidence of fair value delivery (Price & Value)

- Clear client support pathways (Consumer Support outcome)

Yet most mortgage CRM and case management tools do not manage:

- Adviser CPD logs

- FCA competency tracking

- Revenue per adviser

- Internal compliance flags

- HR-linked regulatory documentation

Instead, firms rely on:

- Spreadsheets

- Manual HR files

- Separate CPD platforms

- Email-based documentation

This fragmentation creates risk — especially when firms must evidence outcomes, not just processes.

A Practical UK Example

A growing brokerage firm in Manchester had:

- 8 advisers

- 1 compliance officer

- 2 admin staff

They used:

- A CRM for leads

- A case system for applications

- Excel for CPD

- Separate HR documentation

When the compliance officer conducted an internal review, they discovered:

- Two advisers had incomplete CPD records

- One adviser's revenue reporting didn't match internal logs

- Compliance training documentation was scattered

The systems worked individually.

But there was no centralised governance view.

Real-World Feedback

After introducing a structured governance layer, James Whitaker, Director of a 15-adviser brokerage in London, shared:

“We realised our CRM and case system were fine for clients — but we had very little visibility over our advisers. Once we centralised CPD and revenue oversight, compliance reviews became significantly less stressful.”

That shift wasn't about replacing systems.

It was about connecting them.

Where Traditional Systems Fall Short

This is not a feature failure.

It's a structural limitation.

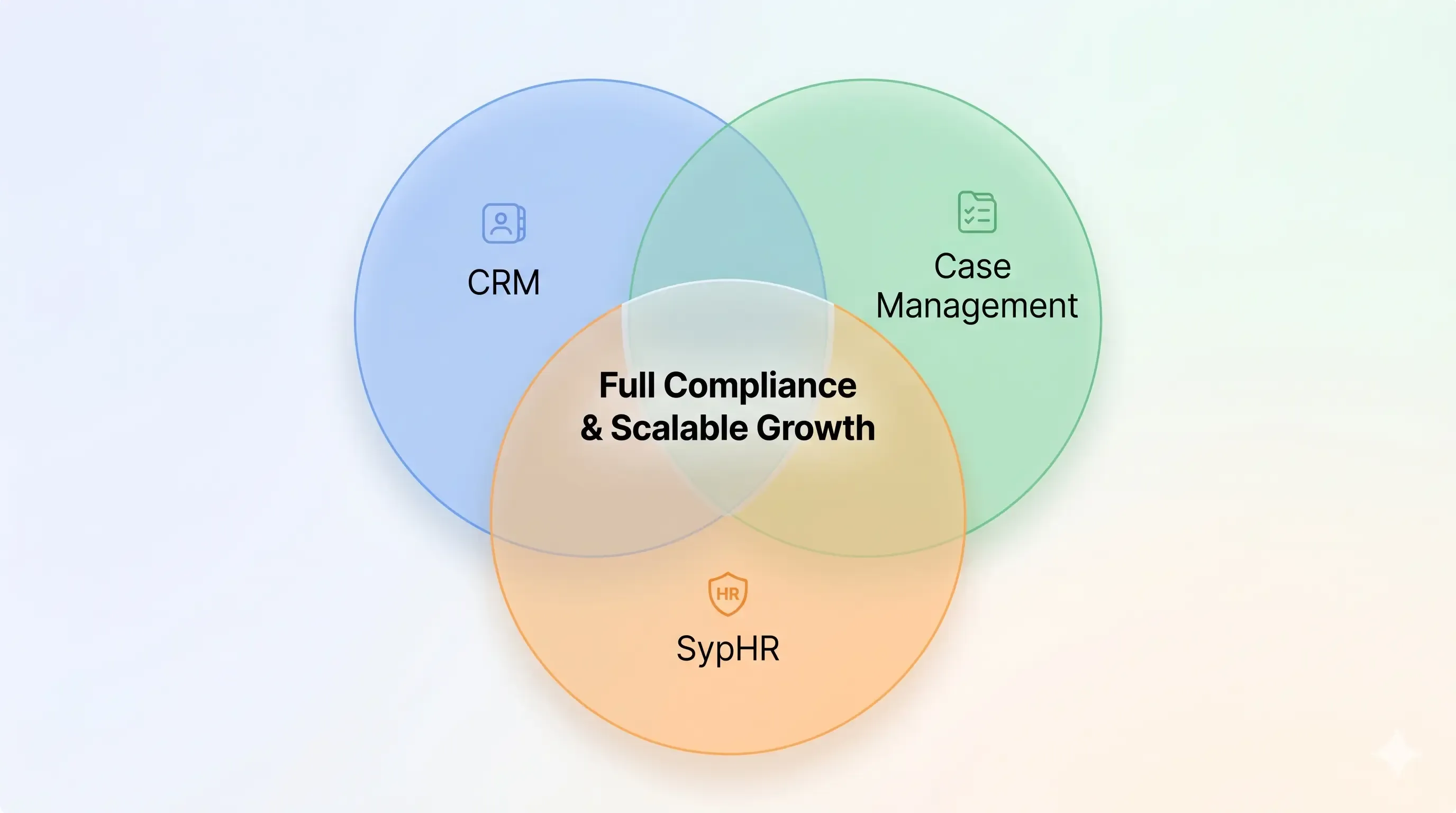

Introducing the Missing Layer: SypHR

While CRM and Case Management handle the “What” and “Who” of a mortgage —

SypHR handles the “How.”

SypHR is designed as a mortgage-specific HR and compliance governance system for UK firms.

It does not replace CRM or case management.

It complements them by addressing what they don't manage:

- FCA CPD tracking

- Adviser competency logs

- Revenue analytics per adviser

- Compliance monitoring

- Internal documentation oversight

- HR-linked regulatory management

- Consumer Duty outcome visibility

In short:

- CRM = client relationship

- Case Management = application workflow

- SypHR = internal governance & adviser oversight

How This Makes a Broker's Life Easier

Instead of:

- Cross-checking multiple spreadsheets

- Manually reviewing CPD records

- Matching revenue to advisers manually

- Preparing for compliance audits reactively

Firms gain:

- Centralised adviser dashboard

- Automated compliance alerts

- Revenue-performance alignment

- Clear audit trail visibility

- Better Consumer Duty evidence

This reduces stress during internal audits and FCA reviews.

Mortgage Broker CRM vs Case Management: The Bigger Picture in 2026

The conversation is evolving.

It's no longer:

- “Do we have a CRM?”

- “Is our case tracking system efficient?”

The real question is:

- “Can we evidence oversight, fair value, and adviser competency across the business?”

In 2026, UK firms that integrate relationship management, case workflow, and internal compliance oversight will operate with:

- Lower regulatory risk

- Better performance visibility

- Stronger revenue intelligence

- More scalable growth

Comparison Table: Traditional Stack vs Integrated Governance

60-Second Internal Governance Audit

Ask yourself:

- Can you instantly see CPD status for every adviser?

- Is adviser revenue automatically tracked against cases?

- Can you evidence Consumer Duty outcomes clearly?

- Are compliance documents centralised?

- Would you feel confident during a surprise FCA audit?

If the answer is “no” to more than two…

There may be operational exposure within your firm.

Key Takeaways

- A mortgage CRM manages relationships.

- Case management tracks application workflow.

- Neither typically manages internal compliance governance.

- UK regulatory expectations now require outcome-based evidence.

- Growing firms need visibility beyond pipeline tracking.

- Understanding Mortgage Broker CRM vs Case Management is only step one.

- The real advantage comes from connecting them with structured governance intelligence.

FAQ

What is the main difference between mortgage CRM and case management?

A mortgage CRM manages client relationships and leads, while case management software tracks application progress and documentation.

Do brokers need both?

Yes. They serve different operational purposes.

Does either system track FCA CPD requirements?

Typically no. That often requires a separate governance or HR-linked system.

How does Consumer Duty affect internal systems?

Firms must evidence fair value, client support, and adviser competency — which requires structured internal oversight.

Can governance systems integrate with CRM and case software?

Yes. Modern governance-focused platforms are designed to complement existing tools rather than replace them.

Conclusion: Growth Requires More Than Pipeline Visibility

Most UK mortgage firms don't struggle because they lack clients.

They struggle because internal oversight, compliance tracking, and adviser performance monitoring are fragmented.

CRM and case management systems are essential.

But they are not the full picture.

In a regulated environment focused on outcomes — not just processes — clarity across client, case, and adviser governance is what protects revenue, compliance standing, and long-term growth.

If your firm is scaling, reviewing how these layers connect may be one of the most important operational decisions you make in 2026.

Related articles

The UK Mortgage Application Process: Step-by-Step Guide for Advisers (With Workflow Comparison, 2026 Remortgage Forecast & Conversion Strategy)

Read more

Mortgage Software for UK Brokers in 2026: How to Handle the 1.8M Remortgage Surge

Read more

Mortgage Eligibility Checks Brokers Should Run Before Applying

Read moreReady to see MAT in action?

Join mortgage professionals already using AI to grow their business.

Book a free demo