Is Your Mortgage Tech Stack Costing You Deals? 5 Revenue Leaks & The AI Fix for 2026

Mortgage Broker Software Explained — And Where Revenue Quietly Leaks

TL;DR

Most mortgage firms use CRM systems, sourcing tools, and criteria databases.

But many are losing deals due to:

- Slow lead response

- Manual qualification

- Criteria misinterpretation

- Missed remortgage triggers

- Fragmented systems

Modern AI-driven mortgage broker software introduces mortgage lead automation and automated remortgage triggers to reduce admin, protect revenue, and improve conversion.

In 2026, the firms using intelligent automation are already moving faster than those relying on manual workflows.

Introduction: Mortgage Broker Software Is Now a Competitive Weapon

The UK mortgage market remains highly active. With over £1.3 trillion in outstanding residential mortgage lending, competition among brokers is intense.

Borrowers expect:

- Near-instant responses

- Clear lender direction

- Fast decision-making

- Structured consultations

Meanwhile, advisers are juggling:

- Compliance documentation

- Multiple active cases

- New enquiries

- Remortgage renewals

In this environment, mortgage broker software is no longer just an admin tool.

It directly affects:

- Conversion speed

- Client retention

- Adviser workload

- Revenue protection

And for many firms, the tech stack that once improved organisation is now quietly limiting growth.

The Changing Landscape of Mortgage Broker Software

Most firms rely on a familiar stack:

- A mortgage CRM

- A sourcing system

- A criteria search database

- Booking tools

- Video platforms

- Email marketing systems

The issue isn't that these tools don't work.

It's that they don't work together.

If they're busy — the process slows.

What Types of Mortgage Broker Software Exist Today?

1. Mortgage CRM Systems

Strengths:

- Centralised records

- Pipeline visibility

- Compliance documentation

Limitations:

- Manual lead follow-up

- No automatic qualification

- No prioritisation logic

- No automated remortgage triggers

A CRM stores opportunity.

It doesn't actively protect it.

2. Criteria & Sourcing Tools

Strengths:

- Lender database access

- Filtering by product features

Limitations:

- Keyword-based searching

- Manual interpretation

- No scenario intelligence

- No real-time eligibility logic

This often leads to over-checking, hesitation, or lender mismatch.

3. Lead Capture & Booking Systems

Strengths:

- Self-booking links

- Calendar integration

Limitations:

- No financial filtering

- No early risk flags

- No intelligent adviser routing

They book time.

They don't optimise it.

The 5 Hidden Revenue Leaks in Most Mortgage Firms

Across firms, the same patterns emerge:

According to Harvard Business Review, responding within five minutes makes firms 21x more likely to qualify a lead.

Yet many mortgage firms still respond manually.

60-Second Mortgage Workflow Audit

Before reading further, ask yourself:

- Are new website or Rightmove/Facebook enquiries contacted within 2-5 minutes — or do they wait until an adviser is free?

- Are applicants pre-qualified for affordability, credit profile, and deposit size before a discovery call is booked?

- Do you have automated remortgage triggers set for 4-6 months before a client's fixed rate expires?

- Does your CRM prioritise leads based on urgency (e.g. purchase vs “just exploring”)?

- If an adviser is in back-to-back client meetings, does your system still engage, qualify, and protect new opportunities?

- Are you proactively reviewing existing clients ahead of product expiry — or relying on diary notes and spreadsheets?

If you answered “no” to two or more…

There's a strong chance your current mortgage broker software is allowing revenue leakage — especially in lead response speed and remortgage retention.

And in today's UK market, the broker who responds first usually wins.

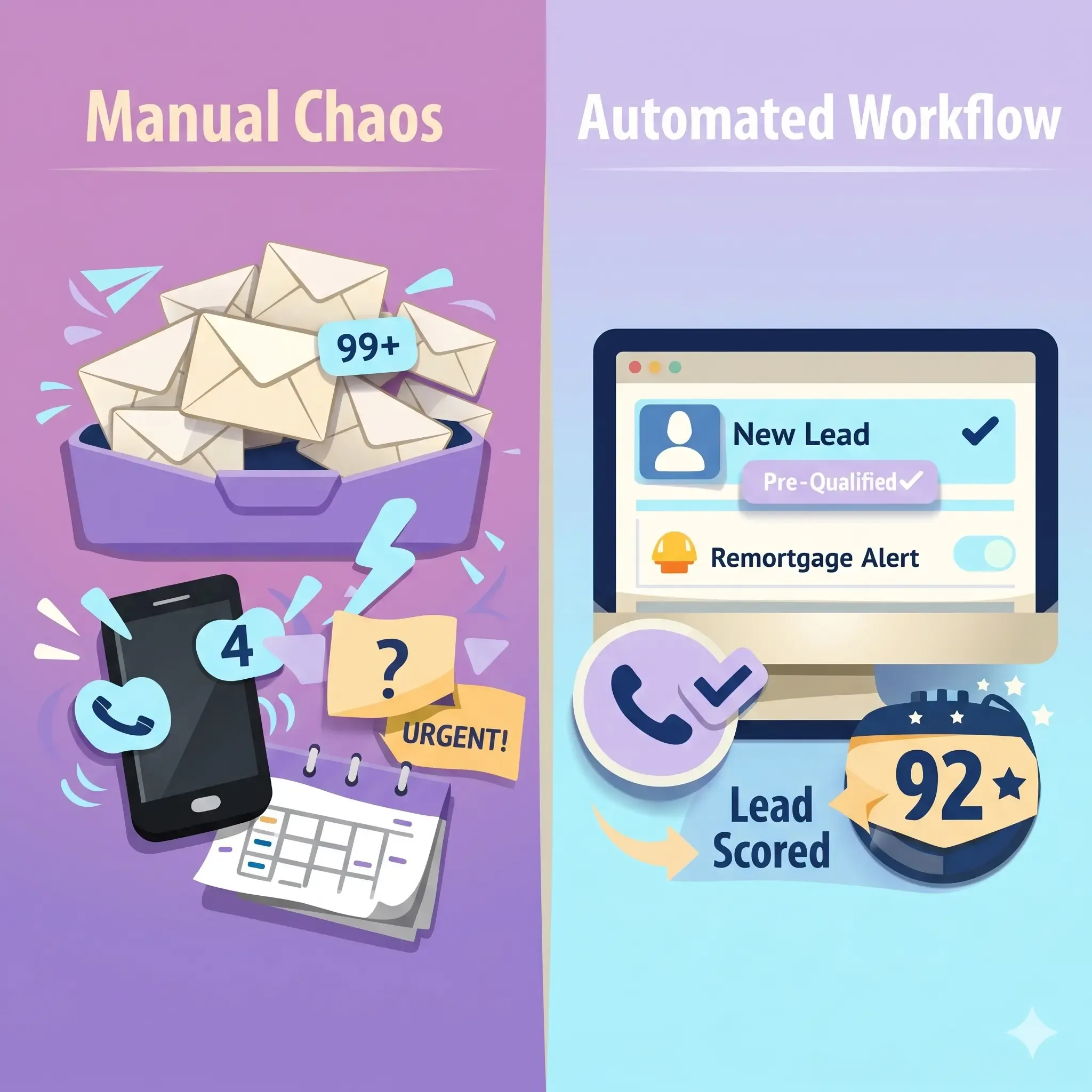

A Practical Example: The Busy Adviser Bottleneck

Let's make this tangible.

A broker receives:

- 15 website enquiries in one afternoon

- 4 social media leads

- 3 remortgage clients nearing expiry

They're in a 90-minute client consultation.

By the time they finish:

- 6 enquiries have already contacted another broker

- 3 weak leads booked time unnecessarily

- 1 remortgage client fixed directly with their lender

This is not uncommon.

Now compare that with an AI-integrated workflow.

Example 1: Mortgage Lead Automation with DealStream

Instead of waiting for manual outreach, DealStream initiates contact instantly.

In one real implementation:

- 15 new website leads were contacted in under 2 minutes

- 11 completed structured pre-qualification calls

- 4 were filtered out before reaching the adviser

- 6 qualified prospects were routed automatically

- 2 remortgage clients were contacted proactively via automated remortgage triggers

All while the broker was still in a meeting.

“I used to lose evenings catching up on enquiries. Now the system handles first contact, and I focus on advising. I've saved 8-10 hours per week.”

This is mortgage lead automation in action.

Example 2: Smarter Criteria Decisions with MyCriteria

Traditional criteria search tools require manual keyword searching.

MyCriteria interprets borrower scenarios conversationally and evaluates eligibility logic in real time.

Instead of:

“Self-employed, 1 year trading, 10% deposit”

The system evaluates:

- Lending appetite

- Risk tolerance

- Eligibility probability

- Scenario fit

Advisers report:

- Faster lender selection

- Increased confidence during calls

- Fewer re-checks and backtracking

AI Workflow vs Traditional Workflow

Comparison Table: Traditional vs AI-Integrated Systems

Why This Matters in 2026

Firms already using intelligent automation are:

- Responding faster

- Booking fewer low-quality meetings

- Protecting renewal revenue

- Reducing adviser burnout

This isn't future technology.

It's current competitive advantage.

If two brokers offer similar advice — the one who responds first and follows up intelligently wins.

How to Choose Mortgage Broker Software for Growth

Ask:

- Does it eliminate admin or just organise it?

- Does it include mortgage lead automation?

- Does it use automated remortgage triggers?

- Does it prioritise by lead quality?

- Does it protect revenue when advisers are busy?

If not — you may be running a 2020 workflow in a 2026 market.

Key Takeaways

- Mortgage broker software directly impacts conversion.

- The biggest revenue leak is delayed response.

- Manual qualification wastes high-value adviser time.

- Automated remortgage triggers protect recurring revenue.

- AI systems are already out-competing manual firms.

- In 2026, the competitive advantage isn't better advice.

- It's better systems behind the advice.

FAQ

What is mortgage broker software?

It includes CRM systems, sourcing tools, criteria databases, booking platforms, and automation systems used to manage client journeys.

What is mortgage lead automation?

Technology that instantly engages and qualifies new enquiries without requiring manual adviser outreach.

What are automated remortgage triggers?

Systems that proactively contact clients months before their current deal expires.

Is AI replacing advisers?

No. It removes repetitive admin so advisers focus on client relationships and strategy.

Conclusion: In 2026, Speed and Structure Win

Most UK mortgage firms don't lose deals because of poor advice.

They lose them because of delayed response, manual filtering, and missed remortgage opportunities.

In today's market:

- Borrowers enquire with multiple brokers.

- Fixed rates expire quietly in the background.

- The adviser who responds first often secures the client.

The difference between a growing firm and a stagnant one isn't just experience — it's workflow design.

Mortgage broker software should not simply record activity.

It should actively protect pipeline value, prioritise serious applicants, and trigger remortgage engagement before competitors do.

Firms already using mortgage lead automation and automated remortgage triggers are:

- Engaging prospects faster

- Reducing wasted appointments

- Retaining more existing clients

- Freeing advisers from repetitive admin

If your current systems rely heavily on manual follow-up, spreadsheets, or delayed outreach, the competitive gap will only widen.

In 2026, the advantage doesn't belong to the busiest broker.

It belongs to the broker with the smartest systems behind them.

Related articles

The UK Mortgage Application Process: Step-by-Step Guide for Advisers (With Workflow Comparison, 2026 Remortgage Forecast & Conversion Strategy)

Read more

Mortgage Software for UK Brokers in 2026: How to Handle the 1.8M Remortgage Surge

Read more

Mortgage Eligibility Checks Brokers Should Run Before Applying

Read moreReady to see MAT in action?

Join mortgage professionals already using AI to grow their business.

Book a free demo