Ensuring Your Mortgage Process Is FCA Compliant | UK Broker Guide

TL;DR

- FCA compliance is about consistent execution, not just knowledge

- Most brokers lose time and accuracy due to manual, fragmented processes

- Key risks include missed fact-finds, weak documentation, and poor audit trails

- Structured workflows improve compliance, efficiency, and client outcomes

- Modern systems help deliver the evidence required under Consumer Duty

Introduction

Ensuring your mortgage process is FCA compliant is no longer just about following rules—it's about proving that your advice process is structured, transparent, and client-focused.

Today, the biggest pressure comes from Consumer Duty.

Firms must now demonstrate:

- Clear consumer understanding

- Fair price and value

- Consistent, evidence-based advice

But here's the reality:

Most compliance failures don't happen because advisors don't know what to do—they happen because processes are inconsistent.

- Questions get missed

- Notes are incomplete

- Documentation is hard to evidence

And that's where risk builds.

The Changing Landscape of Mortgage Compliance

Mortgage compliance is evolving rapidly.

- Regulators expect evidence, not intention

- Clients expect clarity and transparency

- Firms must prove fair outcomes, not just processes

This creates a new challenge:

How do you deliver compliant advice consistently, at scale?

What Types of Tools Exist Today?

Manual Compliance Processes

Strengths

- Flexible

- Advisor-controlled

Limitations

- High risk of human error

- No consistent audit trail

- Difficult to scale

Standard CRM-Based Workflows

Strengths

- Centralised data

- Better organisation

Limitations

- Heavy manual input

- No real-time compliance guidance

- Relies on advisor discipline

Basic Digital Forms & Templates

Strengths

- Structured data capture

- Repeatable

Limitations

- Static

- Not aligned with real conversations

- Still requires manual validation

Strengths Brokers Commonly Appreciate

- Better organisation of client data

- More structured processes

- Improved record-keeping

- Reduced paperwork

Recurring Limitations & Friction Points

- Fragmented systems

- Missed fact-find questions

- Manual note-taking errors

- Weak audit trails

- Time lost chasing missing data

A Practical Problem Many Brokers Encounter

The “Incomplete Fact-Find” Problem

A meeting starts smoothly.

But as the conversation flows:

- Key questions are skipped

- Important details are missed

Later:

- Advisors chase information

- Or proceed with incomplete records

Impact:

- Compliance risk

- Time inefficiency

- Weak audit confidence

The Cost of Inaction

Even small inefficiencies create measurable impact.

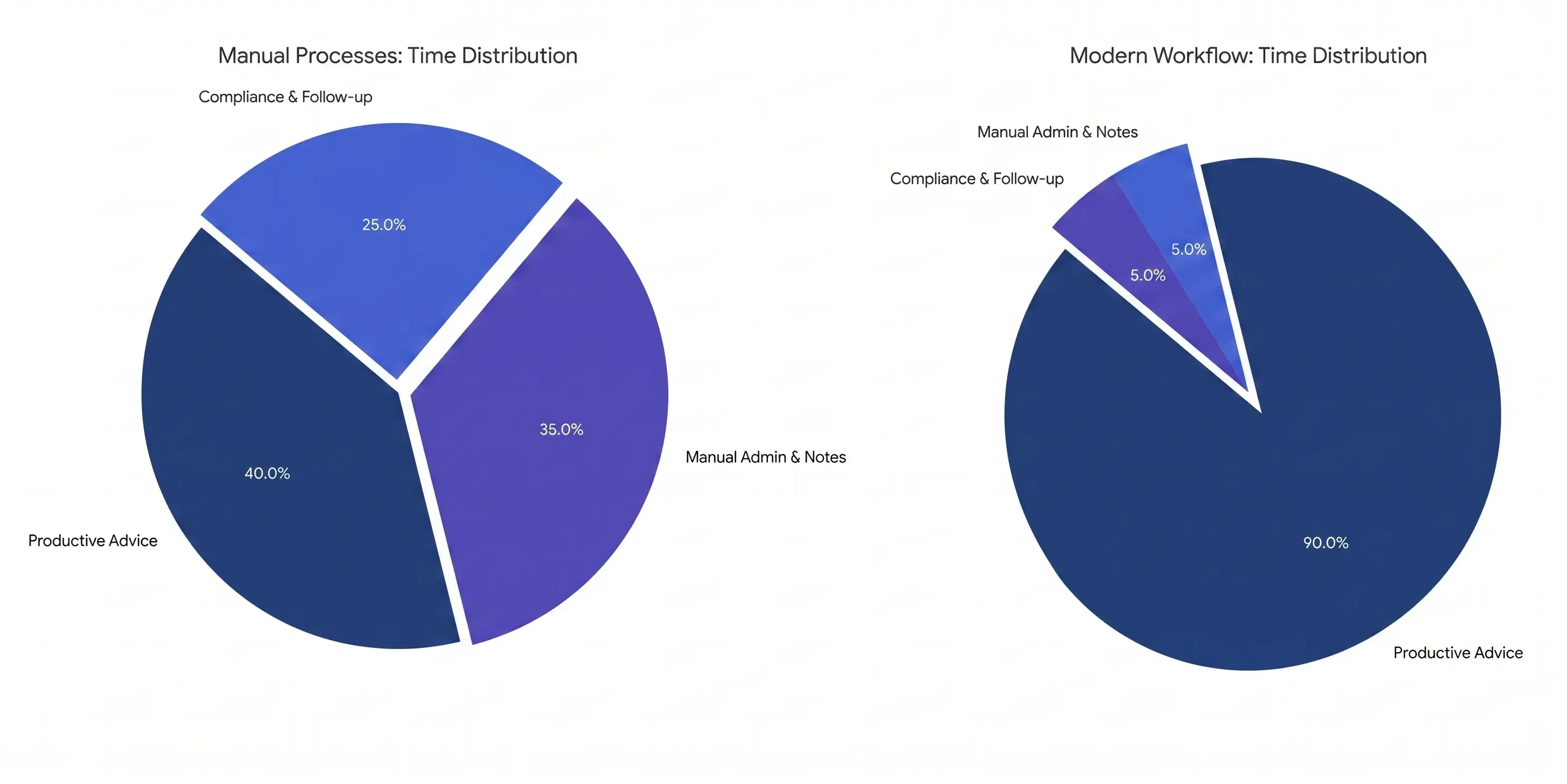

The pie charts below compare the First Meeting Time Breakdown between traditional manual processes and modern workflow systems like EduFlow and Collibry.

Strategic Insights:

- The "Advice Gap" in Manual Systems: In a traditional setup, only 40% of the meeting is actually spent providing advice. The majority of the broker's mental bandwidth is consumed by capturing data and ensuring regulatory compliance in real-time.

- The Modern Shift: By utilizing AI-driven tools, the distribution shifts dramatically. 90% of the time is reclaimed for high-value advisory work and relationship building.

- Reduced Mental Load: Admin and compliance tasks are reduced to just 5% each, as they are automated through transcription and guided digital workflows.

For brokers, this visualization is a powerful lead generation tool because it highlights the direct ROI of your toolkit: more time for clients, less time for paperwork.

What Brokers Often Need But Struggle to Find

- Assurance that nothing is missed

- Real-time support during meetings

- Automatic documentation

- Clear audit trails without extra admin

How Modern Systems Address This Gap

Modern workflows embed compliance directly into the process.

Example: Structured Meeting Intelligence

Tools like

- Captures conversations automatically

- Generates transcripts and summaries

- Tracks fact-find questions in real time

This ensures every conversation is recorded, structured, and auditable.

Example: Guided Workflow Standardisation

Solutions like

- Guides advisors through required steps

- Standardises processes across teams

- Reduces variation and missed actions

Technical Insight (Consumer Duty Focus)

Modern workflow systems don't just improve efficiency—they directly support FCA Consumer Duty requirements:

- Consumer Understanding: Structured conversations ensure clients receive clear, consistent explanations

- Price & Value Evidence: Documented interactions and summaries provide evidence that recommendations are appropriate and justified

This transforms compliance from a reactive task into a built-in, provable process.

Real-Life Example

A broker handling multiple daily meetings:

Before:

- Manual notes

- Missed questions

- Follow-ups required

After:

- Conversations captured

- Fact-find completed during meeting

- Minimal rework

“Our mortgage advisors at WIS Mortgages found that once meetings were properly structured, compliance became far less stressful—we knew everything was being captured properly.”

How to Choose FCA-Compliant Tools: Key Questions

- Does it ensure all required data is captured?

- Does it reduce manual work?

- Can you easily produce an audit trail?

- Does it guide advisors during meetings?

- Where can human error still occur?

Practical Considerations When Evaluating Tools

Comparison of Common Approaches

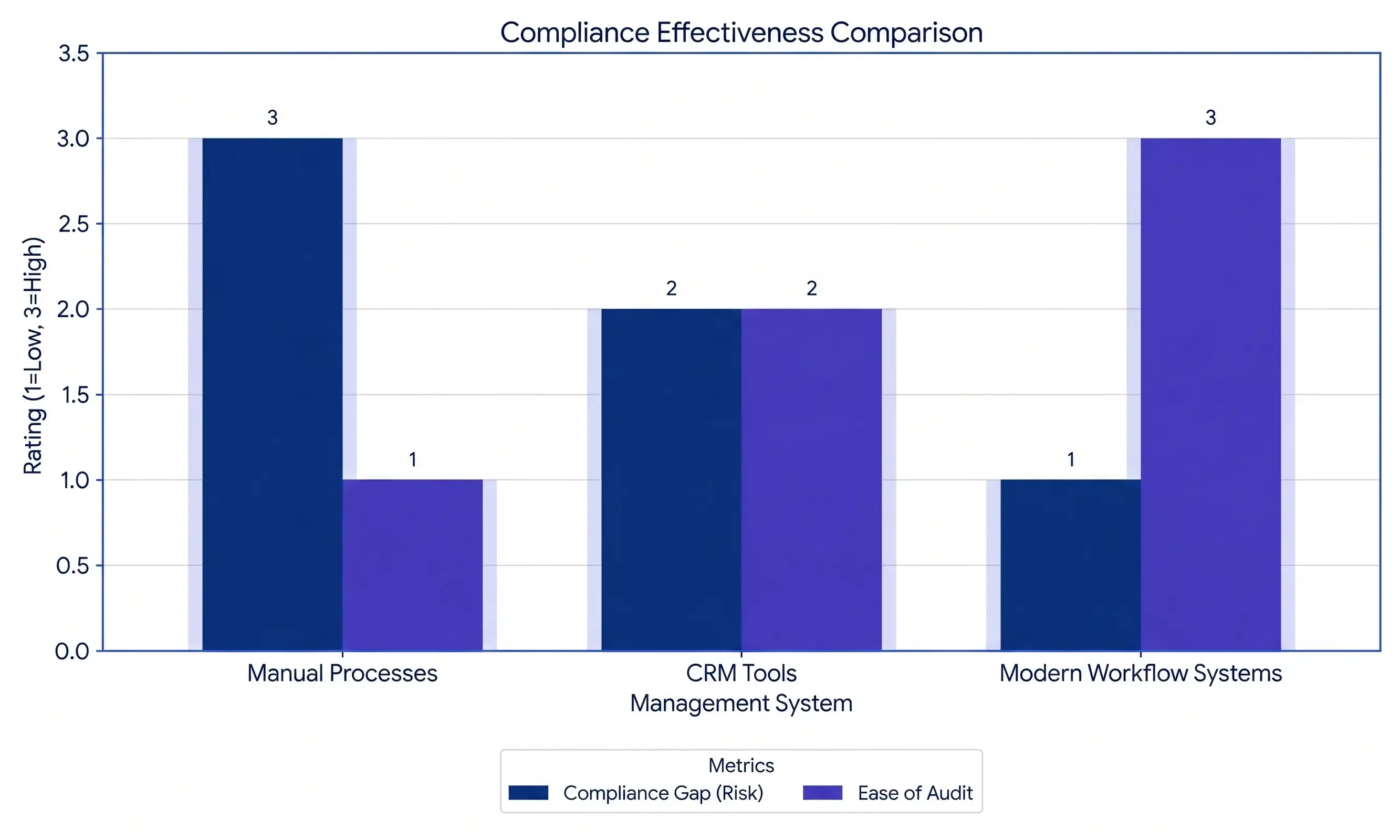

The bar chart below visualizes the Compliance Effectiveness Comparison, contrasting how manual processes, standard CRM tools, and modern workflow systems like EduFlow and Collibry handle regulatory risk and auditability.

Key Observations:

- Manual Processes: Characterized by a high Compliance Gap (Risk) due to human error and reliance on memory, with a low Ease of Audit because records are often fragmented or inconsistent.

- CRM Tools: These represent a middle ground. They improve organization and centralize some data, reducing the risk of lost records, but they still require manual data entry, which limits their auditability and leaves room for human error.

- Modern Workflow Systems: These offer the highest level of compliance effectiveness. By automating data capture and guiding the user through a structured process, they minimize the Compliance Gap (Risk) and create a seamless, high-quality Ease of Audit trail.

This shift from high-risk manual tracking to streamlined automated workflows is a key value proposition for mortgage brokers looking to satisfy FCA requirements and the new Consumer Duty standards with minimal administrative overhead.

Key Takeaways for Mortgage Brokers

- FCA compliance depends on consistent execution

- Most risks come from missed details and fragmented workflows

- Traditional tools organize but don't prevent errors

- Structured workflows improve accuracy and audit readiness

Conclusion

FCA compliance is no longer just about doing the right thing—it's about being able to prove it.

With Consumer Duty now in focus, brokers must show:

- Clear client understanding

- Evidence of fair value

- Consistent, well-documented advice

The firms that succeed will be those that move from:

Ready to reclaim 50% of your meeting time?

See how your current process performs and where compliance gaps are costing you time and risk.

FAQs

What does FCA compliance mean in mortgage advice?

It means ensuring advice is suitable, documented, and supported by a clear audit trail.

What is the biggest compliance risk?

Incomplete fact-finds and poor documentation.

How can brokers improve compliance?

By using structured workflows and ensuring consistency.

Are CRM systems enough?

They help organise data but still rely heavily on manual input.

What role do modern systems play?

They reduce human error and improve consistency by embedding compliance into workflows.

Ready to see MAT in action?

Join mortgage professionals already using AI to grow their business.

Book a free demo