Affordability Stress Testing Mortgage - Preparing for Edge Cases

TL;DR

- Affordability stress testing mortgage is becoming more complex due to non-standard borrower profiles

- Traditional tools struggle with edge cases like self-employed or variable income borrowers

- Brokers face manual recalculations, fragmented workflows, and slower decision-making

- AI-driven systems like Spently & myCriteria enable real-time, dynamic affordability modelling

- Result: Faster decisions, improved accuracy, and better client outcomes

Stop losing complex cases to manual errors. See the AI difference below.

Introduction

The way UK brokers approach affordability stress testing mortgage is evolving rapidly.

Borrowers today are more complex:

- Self-employed

- Multiple income streams

- Changing financial commitments

Meanwhile:

- Lenders demand precision

- Clients expect speed

- Regulations require robust stress testing

The reality?

Most traditional tools were never built for this level of complexity.

The Changing Landscape of Mortgage Affordability Assessment

What's Driving the Shift?

- Interest rate volatility → Higher stress testing requirements

- Rise in non-standard income → More complex affordability logic

- Stricter lender criteria → Increased rejection risk

- Client expectations → Faster turnaround times

UK Finance reports that 30%+ of UK applicants fall into non-standard income categories, making affordability assessments significantly more complex.

What Types of Affordability Tools Exist Today?

Static Calculation Tools

✔ Quick for simple cases

❌ Break under complex scenarios

Criteria-Based Systems

✔ Help identify lenders

❌ Disconnected from affordability calculations

Spreadsheet Workflows

✔ Flexible

❌ High manual effort + high error risk

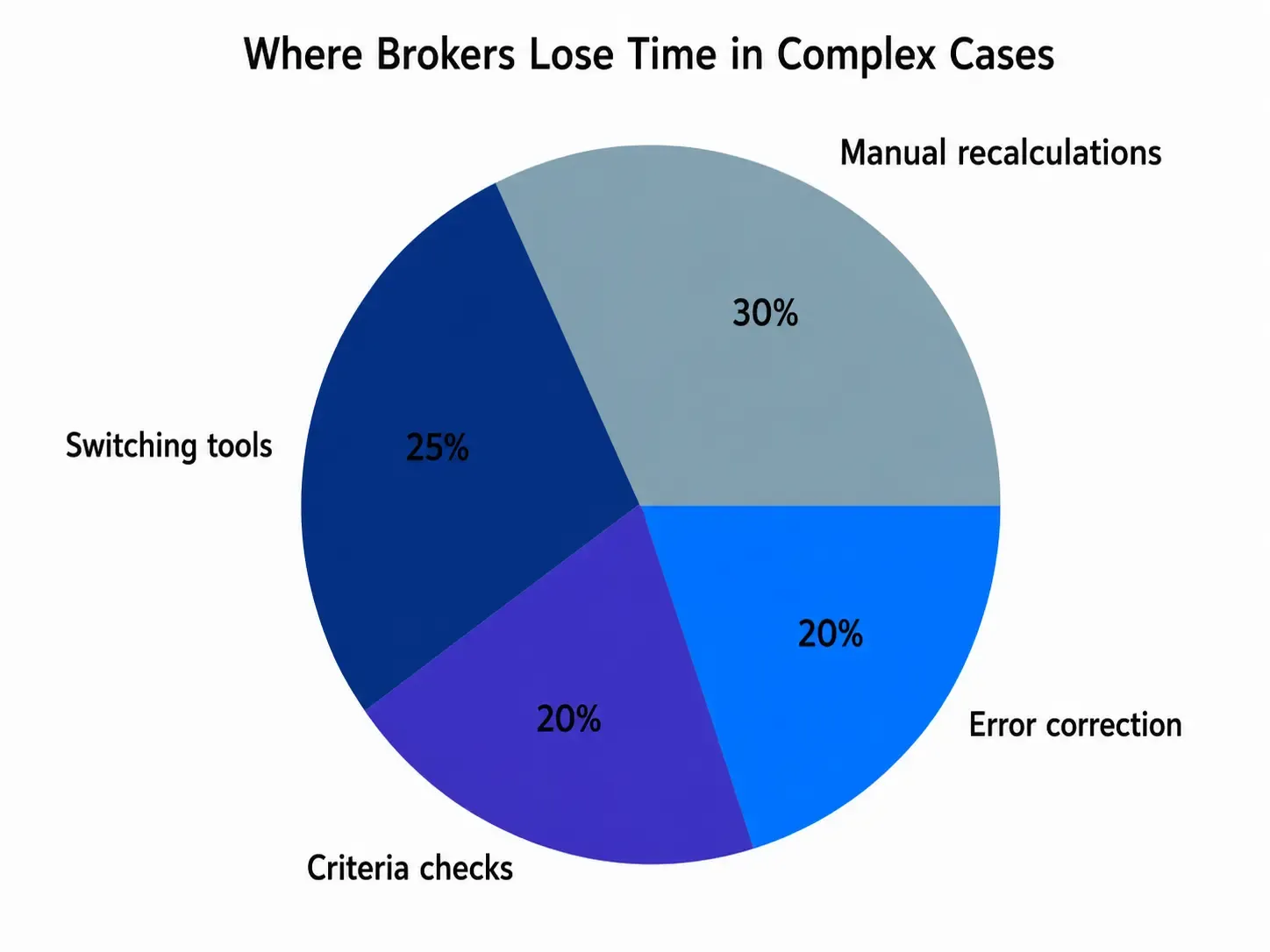

Recurring Limitations & Friction Points

Most time in complex cases it isn't spent advising clients it's lost to manual recalculations, tool switching, and error correction. These inefficiencies not only slow decisions but also increase the risk of costly mistakes

A Practical Problem Many Brokers Encounter

The Edge Case

A UK borrower:

- Newly self-employed

- Variable income

- Existing credit commitments

This isn't an unusual case it's becoming the norm.

More than one-third of UK mortgage applications now involve non-standard income structures, requiring deeper affordability analysis.

Traditional Workflow

- Manual income interpretation

- Multiple recalculations

- Cross-referencing criteria

At each step, the broker is forced to pause, recheck, and validate turning what should be a quick assessment into a time-consuming process.

The Impact

- Time Drain: 45-60 minutes per complex case (industry workflow average)

- Error Exposure: Manual processes introduce an estimated 30-40% risk of calculation or data-entry errors in multi-step scenarios

- Client Impact: Delays increase drop-off risk and reduce conversion rates

The challenge isn't just complexity—it's the lack of tools designed to handle it efficiently.

What Brokers Often Need But Struggle to Find

- Real-time affordability modelling

- Integrated lender + affordability insights

- Automated scenario testing

- Reduced manual workload

How Modern AI-Driven Systems Address This Gap

Dynamic Affordability Modelling

- Reduce Decision Time: From 45 minutes → under 10 minutes

- Integrated Criteria + Affordability

- Improve Accuracy: Align affordability with lender criteria instantly

How AI Actually Works

Modern systems go beyond generic automation by combining multiple technologies:

- Natural Language Processing (NLP): Extracts structured data from documents like bank statements and income records

- Predictive Modelling: Simulates affordability across 50+ lender-specific stress-rate variables simultaneously

- Rule-Based Engines: Apply lender criteria dynamically and consistently

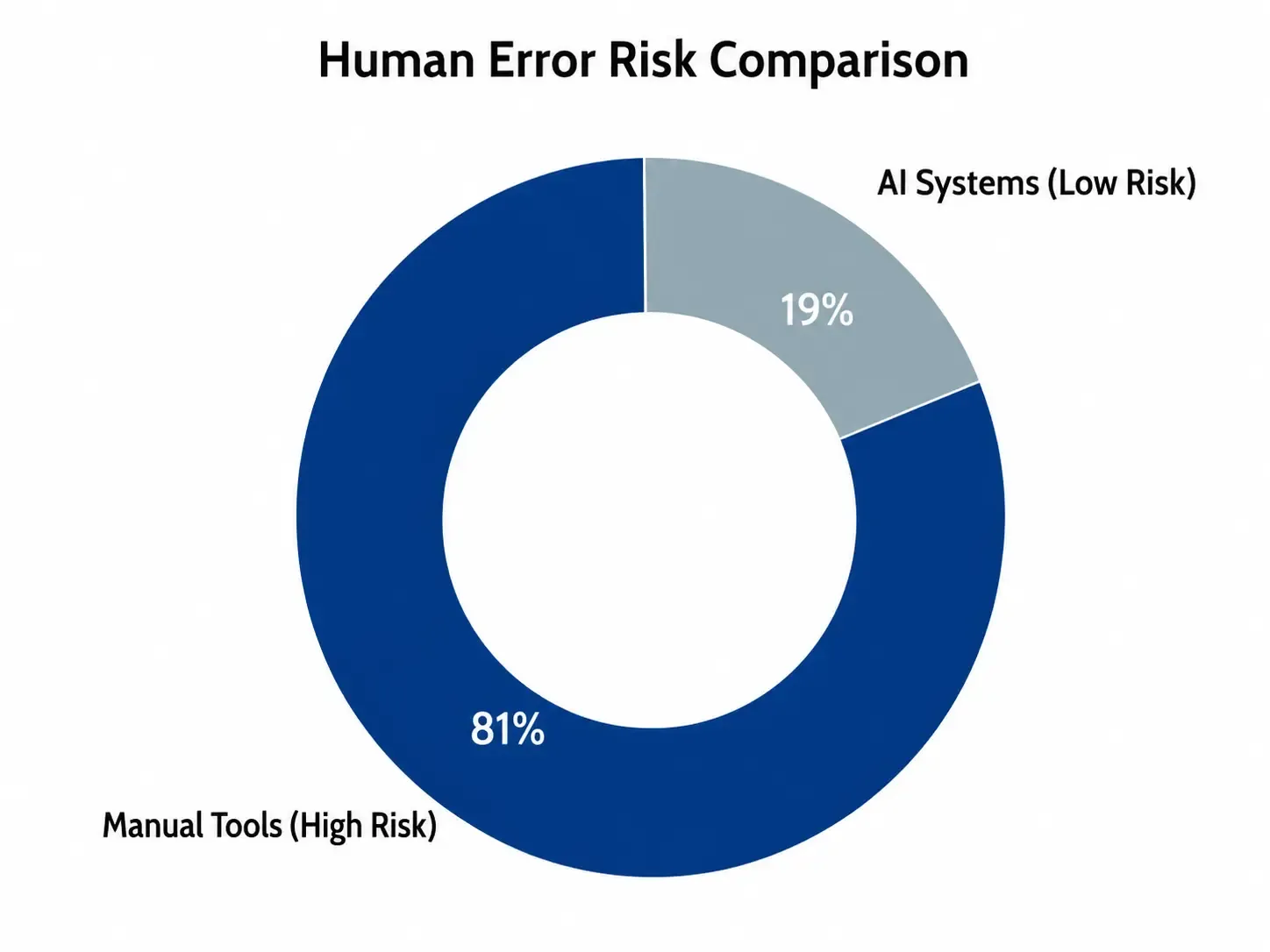

Error Risk Comparison

Manual affordability assessments rely heavily on repeated inputs, recalculations, and cross-checking—each step increasing the likelihood of errors. AI-driven systems significantly reduce this risk by automating data extraction and applying consistent logic across every scenario.

Outcome

More reliable, faster, and data-driven decision-making

Example: Spently & myCriteria in Practice

From your internal ecosystem

- Spently → Streamlines affordability workflows

- myCriteria → Enhances lender matching

Combined Impact

- Automate affordability adjustments

- Eliminate manual recalculations

- Deliver instant lender matches

Real Outcome

- Faster Decisions: 45 mins → <10 mins

- Higher Accuracy: Better lender alignment

- Improved Client Experience: Faster responses

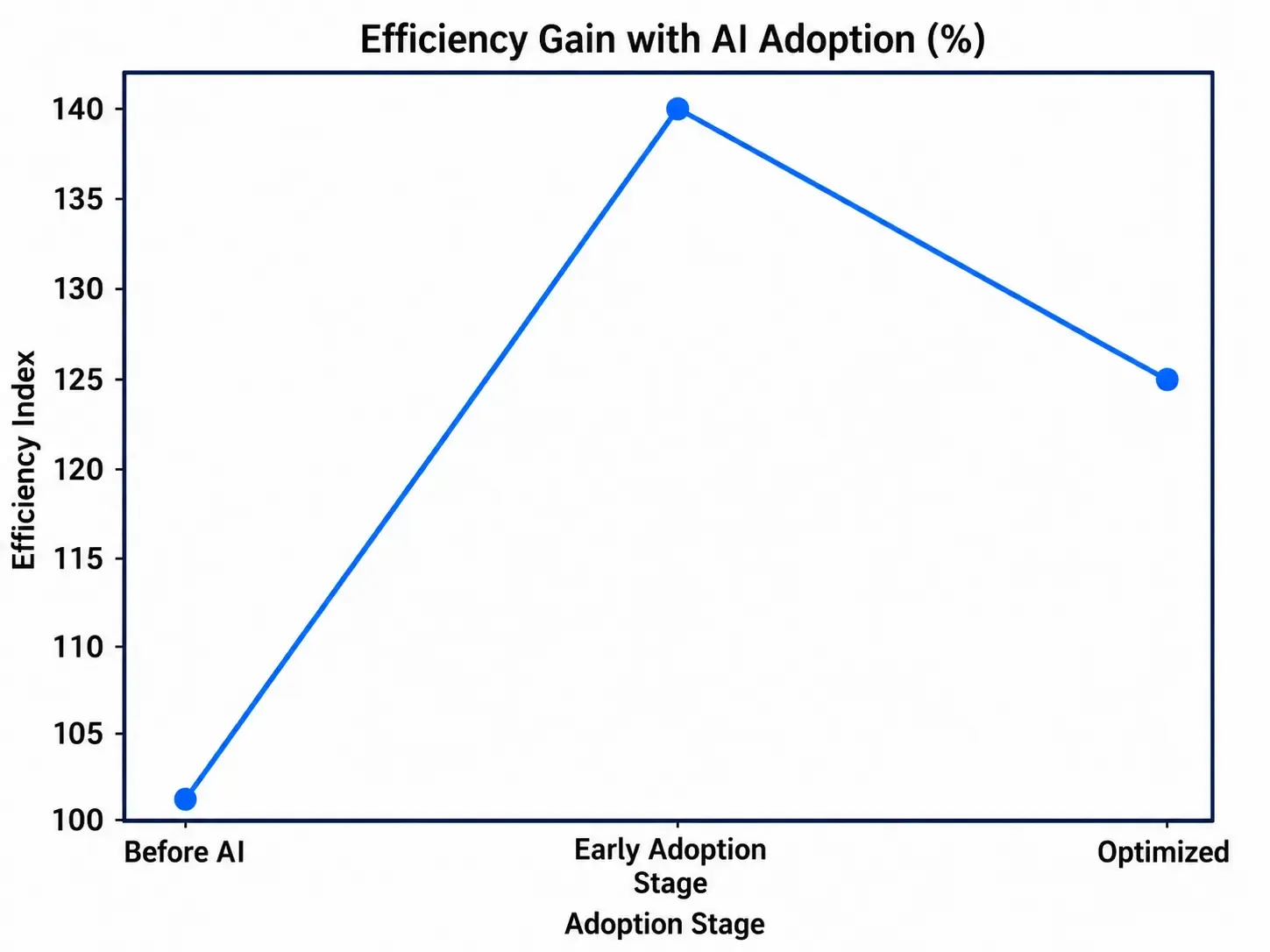

What Happens After You Adopt AI?

This chart illustrates how efficiency improves as brokers adopt AI-driven affordability tools. After an initial adjustment period, workflows become significantly faster and more streamlined, typically delivering up to 25% gains in processing efficiency.

Try It Yourself

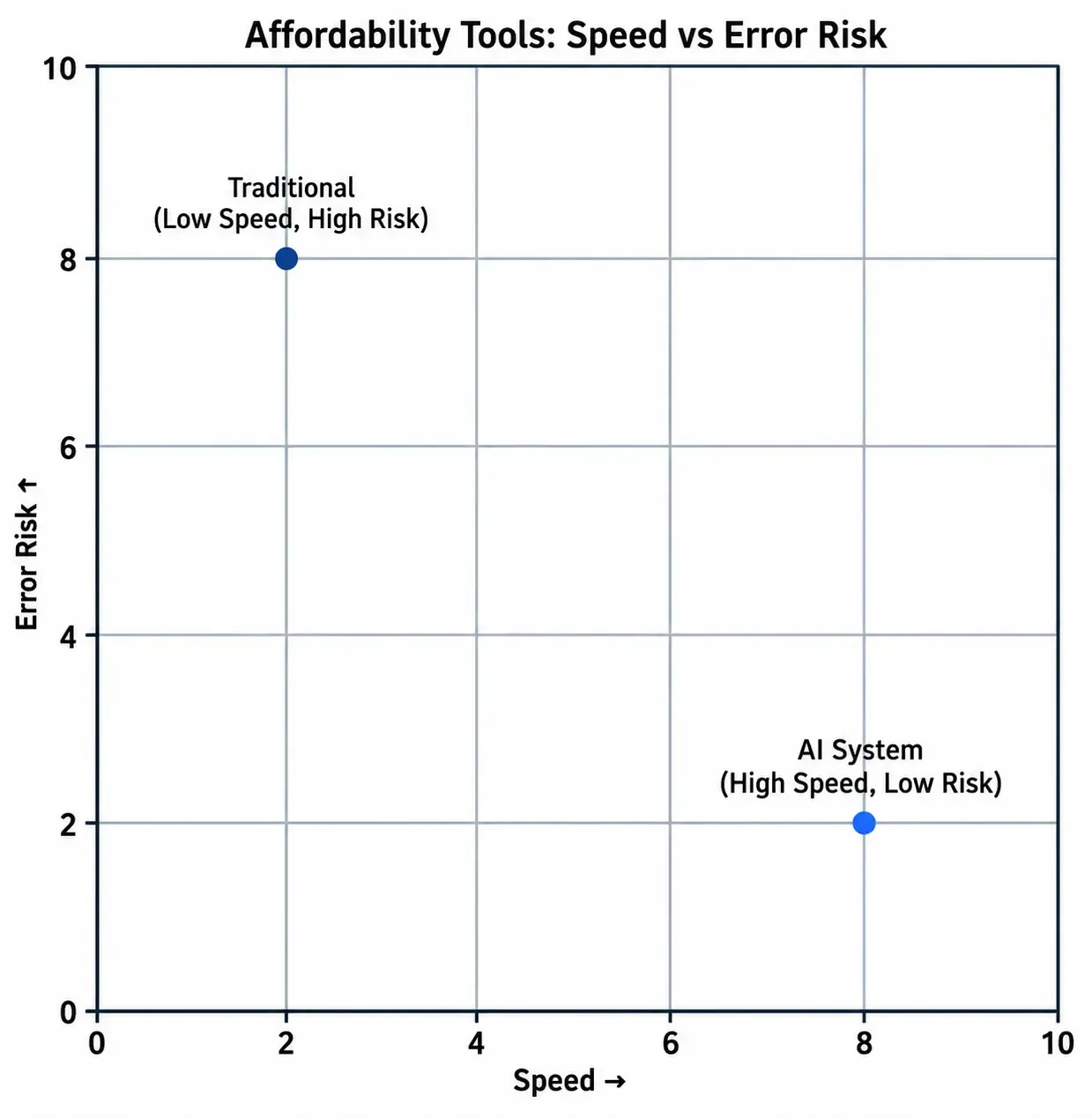

Traditional vs AI Affordability Tools

While both traditional and modern systems aim to assess affordability, their performance differs significantly when it comes to speed and accuracy especially in complex cases.

This comparison shows how traditional affordability tools and AI-driven systems differ in terms of speed and error risk. Manual processes tend to operate in a lower-speed, higher-risk zone, while AI-enabled systems shift affordability assessments toward faster, more reliable outcomes.

Data Representation

How to Choose Affordability Tools

- Does it reduce manual work?

- Can it handle edge cases dynamically?

- Does it provide insight, not just outputs?

Practical Considerations

- Integration

- Usability

- Scalability

- Accuracy

Key Takeaways

- Affordability stress testing is more complex than ever

- Traditional tools struggle with edge cases

- Manual workflows create risk and inefficiency

- AI systems deliver speed, accuracy, and confidence

FAQ

What is affordability stress testing mortgage?

It evaluates whether borrowers can afford repayments under stressed conditions.

Why are edge cases difficult?

They involve variables traditional tools cannot model effectively.

How do AI tools improve this?

They automate calculations and simulate multiple scenarios instantly.

Conclusion

Affordability stress testing is no longer just a calculation it's a competitive advantage.

Brokers who adapt to:

- Faster workflows

- Smarter tools

- Data-driven decisions

…will win more complex cases.

Solutions like Spently and myCriteria show what's possible when affordability analysis evolves from manual effort to intelligent decision-making.

Ready to see MAT in action?

Join mortgage professionals already using AI to grow their business.

Book a free demo